Fundamental Factors Driven Long-Short Hedge Fund Strategy

Fundamental Factors Driven Long-Short Hedge Fund Strategy

MP4 | Video: AVC 1280x720 | Audio: AAC 44KHz 2ch | Duration: 2 Hours | Lec: 16 | 452 MB

Genre: eLearning | Language: English

MP4 | Video: AVC 1280x720 | Audio: AAC 44KHz 2ch | Duration: 2 Hours | Lec: 16 | 452 MB

Genre: eLearning | Language: English

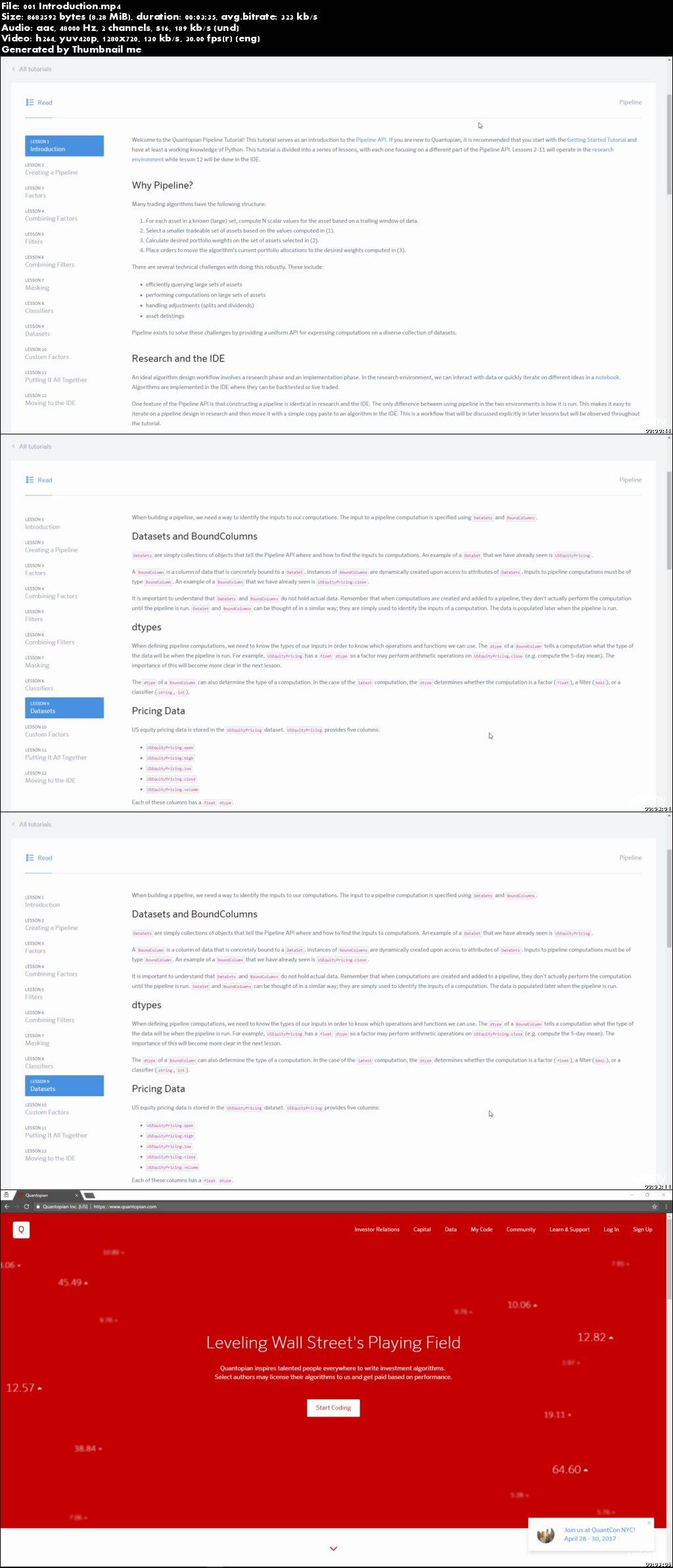

Making use of the Quantopian Pipeline API to select security dynamically for your algo

In this course you will learn how to utilise the Quantopian Pipeline API to create your own algorithm.

The course will cover the basics and purpose of Quantopian Pipeline, and how you can make use of it to dynamically select specific sets of assets to trade. The Quantopian Pipeline works seamlessly between the research platform and IDE, the course will highlight the similarities and differences of the working of Pipeline in each platform.

Starting with the steps needed to run a Pipeline to the different computations that can be expressed in Pipeline, the course will demonstrate how one can create and run a Pipeline and identify the main components in order for Pipeline to run successfully. Factors, filters, and classifiers will be covered.

Quantopian provides a diverse range of datasets to break down the traditional barriers to assist algorithm writers to develop institutional strengths algorithm. The Quantopian Pipeline also allows writers to develop their own Custom Factors.

Please note that this course will not teach you how to use Python. It assumed a certain level of competency with Python and in particular Jupyter Notebook. The course teaches you how to make use of the Quantopian Pipeline API to develop algo. It does NOT cover trading strategies nor does it teach you how to make money. This course is provided for educational purpose.

Fundamental Factors Driven Long-Short Hedge Fund Strategy

Please update your winrar to avoid getting extract error