Basic Inventory Control ver.5.0.122

Basic Inventory Control ver.5.0.122 | 5,75 MB

Inventory control is a process by which an organization keeps track of its product counts and ensures physical product counts match what is recorded in its books. From a financial standpoint, inventory is the most valuable asset of an organization engaged in buying, selling, manufacturing or otherwise handling of tangible goods. For many organizations, proper management of inventory is pivotal to customer satisfaction and long-term success. The following are few of the challenges faced by organizations in the realm of inventory control.

Challenges of Inventory Control

* Companies usually handle a large number of products. Units of products move rapidly as new orders are received, products are returned, products are drop-shipped, out of stock products are backordered or products are earmarked for a delayed shipment. The sheer volume of items makes the task of monitoring inventory complicated.

* In order to minimize cash tied up in inventory and to reduce inventory handling costs, an organization must know its current inventory count accurately at all times. This information is essential in knowing when to re-order products that are out of stock or are about to go out of stock. There are significant costs associated with carrying too much inventory such as cash tied up in slow moving inventory, inventory storage and handling costs, spoilage and obsolescence. On the other hand, carrying too few units could result in stock-outs and loss of sales or production stalls. The ultimate goal is not to order too many or too few goods. The more accurate the inventory count, the better an organization is in a position to order an Economic Order Quantity (EOQ) that minimizes inventory costs and helps negotiate best price discounts.

* Cost of goods sold is the largest expense for businesses that deal with tangible products. Inventory control must track the number of units and the monetary value of the inventory. Companies need an accurate cost of goods sold in order to calculate their profit margins per product or across products.

* Companies need to safeguard their inventory against pilferage, outright theft and loss. A process needs to be in place that keeps track of inventory and helps ensure the physical count matches product count recorded in company books. Sound inventory control is an excellent deterrent against pilferage.

Why Basic Inventory Control?

* Basic Inventory Control keeps an accurate count of products and generates list of products that need to be reordered.

* Basic Inventory Control is a perpetual inventory control system. That is, BIC provides up to date, accurate count of units in stock. Contrast a perpetual inventory control system with a periodic inventory control system where inventory counts are usually updated periodically at month, at quarter or at year end.

* Basic Inventory Control maintains a physical and available inventory count. Physical units in stock refer to products physically present on premises. Available units in stock includes physical units in stock as well as units on order. Further, BIC allows allocation of units for shipment. Allocated units are excluded from available units in stock but included in physical inventory.

* Basic Inventory Control automatically calculates the average unit cost of units as units enter and leave inventory. Average Costing method removes peaks and valleys in inventory cost as units acquired at high and low price levels average out. Cost of goods is automatically calculated on product by product basis as well as in aggregate.

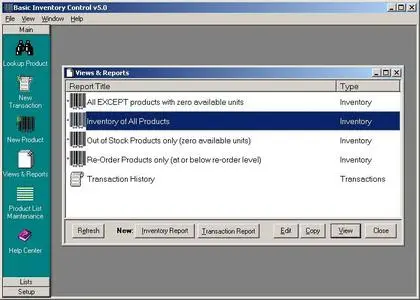

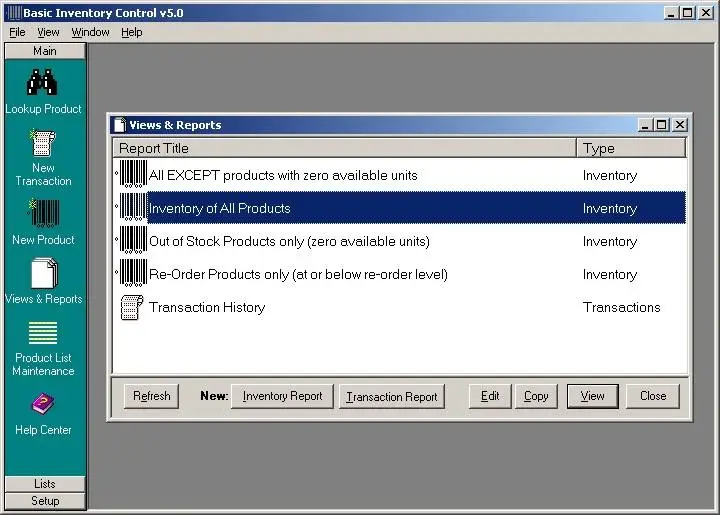

* Basic Inventory Control provides customizable inventory and transactions report for cross-checking physical inventory with inventory recorded by Basic Inventory Control. Each inventory transaction is recorded providing a complete audit trail.