PluralSight - Understanding and Applying Financial Risk Modeling Techniques

Understanding and Applying Financial Risk Modeling Techniques

.MP4, AVC, 1280x720, 30 fps | English, AAC, 2 Ch | 2h 52m | 378 MB

Instructor: Vitthal Srinivasan

.MP4, AVC, 1280x720, 30 fps | English, AAC, 2 Ch | 2h 52m | 378 MB

Instructor: Vitthal Srinivasan

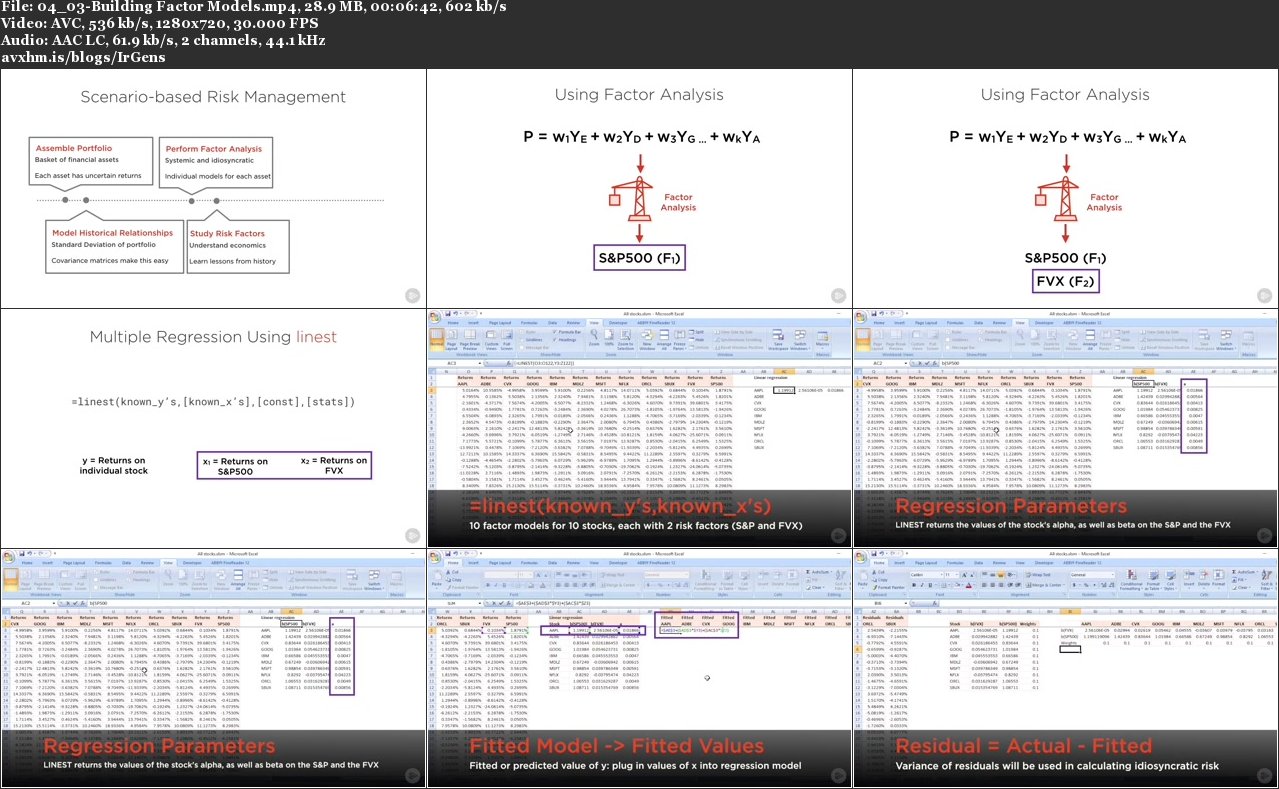

Financial risk modeling is at the intersection of two hot trends: Fintech and Big Data. This course covers three financial risk modeling techniques: covariance matrices, factor models, and value-at-risk.

Financial risk modeling is back in the limelight these days because of its place at the intersection of two hot trends: Fintech and Big Data. Enthusiasm about the intersection of technology and finance is tempered by caution born from past financial risk management failures, such as those witnessed during the Subprime Crisis. In this course, Understanding and Applying Financial Risk Modeling Techniques, you'll learn the details of three related financial risk modeling techniques: covariance matrices, factor models, and value-at-risk. First, you'll discover risk, uncertainty, and standard deviation. Next, you'll explore the role of covariance matrices in modeling risk. Then, you'll go through building scenario-based stress tests using factor models. Finally, you'll learn how to implement a robust risk modeling approach using Excel, VBA, R, and Python. By the end of this course, you'll have a good understanding of how financial risks of all types can be quantified and modeled.

PluralSight - Understanding and Applying Financial Risk Modeling Techniques